A home inventory is one of those tasks everyone agrees is sensible and almost nobody does, until disaster strikes. After a fire, flood or burglary, an insurer asks you to list everything you lost and prove its value. From memory, under stress, that is nearly impossible.

This free template lets you document your belongings calmly, in advance. So you record each item with its brand, serial number, purchase price and current value. As a result, you hold the proof an insurer needs, and a claim becomes a form-filling exercise rather than a guessing game.

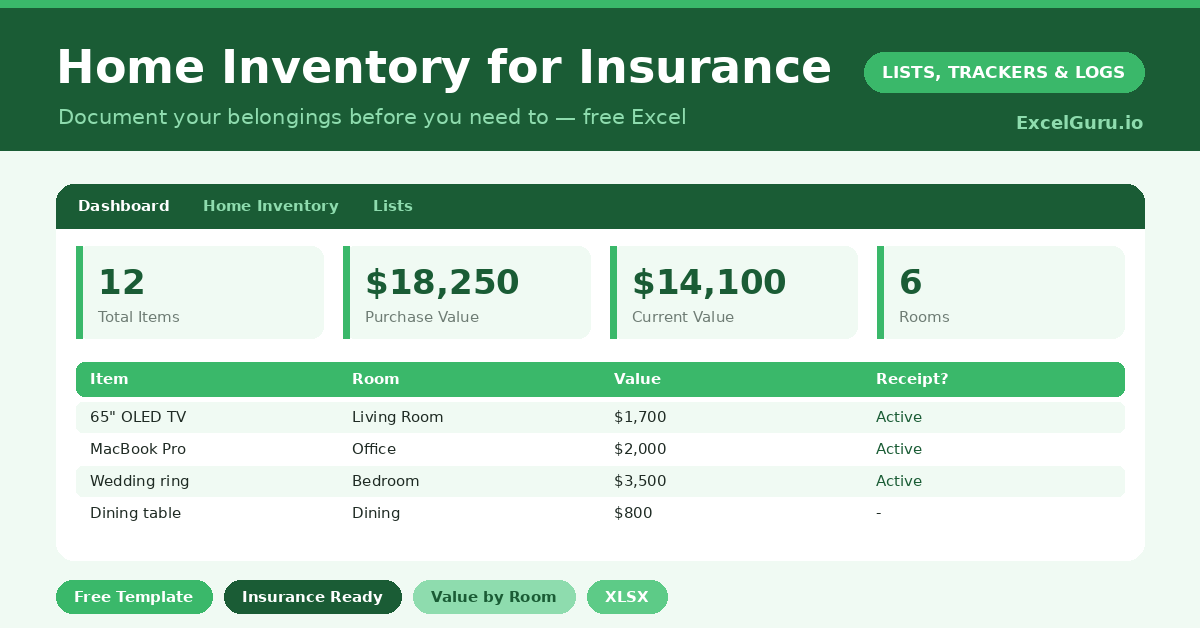

What does the home inventory include?

The template is one detailed list feeding a summary dashboard. Dropdowns keep categories and rooms tidy. In short, you get the following:

- An inventory list with the item, category, room, brand or model, serial number, purchase date, purchase price, estimated value and a receipt flag.

- Drop-down lists for category and room, so entries stay consistent and sortable.

- A receipt column, so you can see which items have documentation to back them up.

- A dashboard showing total items, total purchase price, total estimated value, items with receipts, the number of rooms and your single most valuable item.

Which formulas power the home inventory?

The dashboard does the totting up for you. A SUM of the purchase prices and another of the estimated values give you the headline figures your insurer cares about. So you can see the total worth of your possessions at a glance.

A COUNTIF counts how many items have a receipt logged, which is a useful measure of how claim-ready you are. A clever INDEX and MATCH pair then finds your single most valuable item by its estimated value. Because it all updates as you add items, the picture of your possessions stays current.

Why keep a home inventory?

The obvious reason is insurance. A documented inventory turns a stressful, contested claim into a smooth one, because you can prove what you owned and what it was worth. So you are far more likely to be paid fairly and quickly.

There are quieter benefits too. The exercise often reveals you are under-insured, since most people badly underestimate the total value of their belongings. It also helps with estate planning and house moves. Furthermore, photographing items as you log them makes the record even stronger. In short, a few hours now can save you a great deal later.

What does the dashboard reveal?

The dashboard gives you a clear financial picture of your home. The total estimated value is the number that matters most, since it tells you whether your contents cover is actually enough. So you can adjust your policy before a loss, not after.

The total purchase price shows what you have spent over the years, which is often eye-opening. The receipts count highlights where your documentation is thin, so you know what to shore up. The most-valuable-item figure flags the possessions worth protecting most carefully. In short, the dashboard turns a long list into actionable insight.

How do you build it?

Work room by room, because that is the easiest way to be thorough. So start in the living room, list everything of value, then move on. Capture the brand, model and serial number for electronics and appliances, since insurers often want them.

Record the purchase price where you remember it, and a realistic current value for each item. Tick the receipt column wherever you have proof, and store those receipts safely. Then keep a copy of the whole file off-site or in the cloud, because an inventory destroyed in the same fire is no use. Update it once a year, and after any big purchase.

How do you customize it?

Edit the categories and rooms on the Lists tab to match your home. Additionally, you can add columns for a photo reference, a warranty link, or the replacement cost as opposed to the current value. Some people add a priority flag for irreplaceable items. The template scales easily from a small flat to a large, fully furnished house.

What mistakes should you avoid?

The first mistake is only listing the obvious big-ticket items. The total value of clothing, kitchenware and small electronics is far higher than people expect, so be thorough. The second mistake is keeping the only copy at home, where the same disaster could destroy it.

Always store a backup off-site or in the cloud. Finally, do not create it once and forget it. Possessions change, so update the inventory yearly and after major purchases. An out-of-date inventory is better than none, but a current one is what truly protects you.

Frequently asked questions

Why do I need a home inventory for insurance?

After a loss, insurers ask you to list and value what you owned. A pre-prepared inventory provides that proof, so your claim is processed fairly and quickly rather than disputed from memory.

What details should I record for each item?

At minimum, the item, its value and the room. For electronics and appliances, add the brand, model and serial number, and tick the receipt column wherever you have proof of purchase.

How does it find my most valuable item?

An INDEX and MATCH formula scans the estimated-value column for the highest figure and returns that item’s name, so you can see at a glance which possession is worth protecting most.

Work through your home room by room, record values and serial numbers, and keep a copy in the cloud. The dashboard then shows whether your cover is enough. A home inventory is a dull afternoon’s work that, on the worst day, turns a nightmare claim into a simple, fair one.